1. Reverse Charge

The reverse charge mechanism is a simplification measure which shifts the liability for the payment of VAT on a particular transaction from the supplier to the customer.

For instance, when a taxable person established and registered for VAT purposes in Italy provides legal services to another taxable person established and registered for VAT purposes in Malta, in terms of Article 44 of Council Directive 2006/112/EC, the transaction takes place where the customer is established i.e., in the case under review, Malta. As a result, The Italian taxable person will not charge Italian VAT but by virtue of Article 196 of the same Directive mentioned above, the liability for payment of the VAT is shifted on the customer i.e., the Maltese taxable person. In this regard, the Maltese taxable person will have to account for VAT via the reverse charge mechanism.

For VAT reporting purposes the taxable value of the transaction has to be recorded in Box 3 of the Malta VAT Return and reverse charged in Box 6. In addition, the taxable value has to be declared in Box 9A (unless exempt) and to the extent that the taxable person has a right to deduct input VAT, the input VAT should be recorded in Box 13A.

Changes to the Malta VAT Return to reflect the above

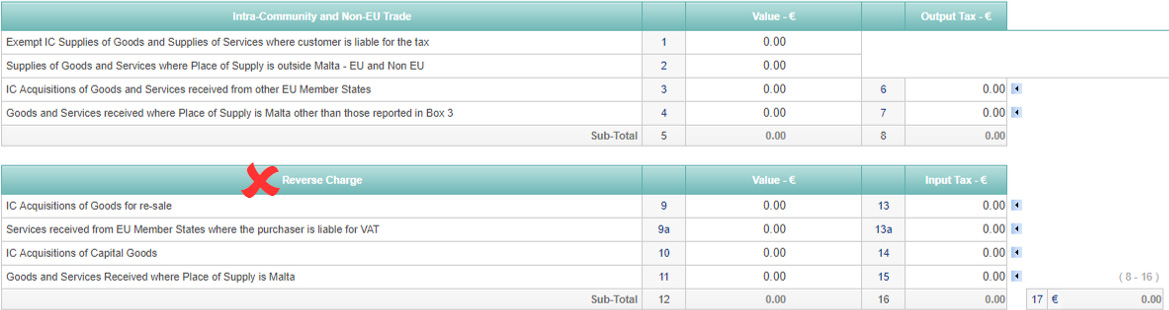

Whilst the reverse charge is correctly reported in Box 6 (in case of the above scenario), the heading of ‘Reverse Charge’ was incorrectly referenced in the Malta VAT Return which seemed to imply that the reverse charge should be reported in boxes 13 to 15. Therefore, for the purposes of clarity, the heading of the section which previously read ‘Reverse Charge’ now reads ‘Deductions of Self-Charged VAT’.

Please see the below screenshot.

2. Intra-Community Acquisition of Goods

In addition to the above, the text in Box 9 of the Malta VAT return, which previously read ‘IC Acquisitions of Goods for re-sale’ now reads ‘IC Acquisitions of Goods excluding Capital Goods’. Therefore, in this case, any intra-Community acquisitions of goods made for business purposes or for resale, will be reported in this Box. If, on the other hand, a taxable person makes an intra-Community acquisition of Goods, which falls within the remit of the definition of capital goods, then such transaction will be reported in Box 10 with the right of deduction exercised by reporting the value in Box 14 of the return.

3. Updated VAT Return