On the 24th of April 2024, a milestone was achieved in the realm of corporate responsibility as the European Parliament formally adopted the Corporate Sustainability Due Diligence Directive (CSDDD). With its formal adoption, the EU underscores its commitment to fostering sustainable business practices and ethical standards.

What is the CSDDD?

The CSDDD mandates that companies and their supply chain prevent, mitigate or cease adverse impacts on human rights and the environment. This includes addressing issues like slavery, child labour, labour exploitation, biodiversity loss, and pollution. Its objectives encompass better human rights and environmental protection, improved living standards, and justice for affected parties. The CSDDD establishes a baseline for EU Member States to incorporate into their legislation. Member States are obligated to develop or revise existing laws to align with the objectives and scope of the CSDDD. While the directive outlines minimum requirements, Member States retain the flexibility to enhance due diligence standards or expand the scope to include activities presently outside the directive’s purview.

Requirements of the CSDDD

The CSDDD establishes foundational requirements for companies to establish and execute suitable measures for conducting due diligence. This ensures that companies can proficiently recognise and tackle adverse human rights and environmental impacts. These measures include but not limited to the following:

- Integrating due diligence into policies and risk management systems,

- Monitoring the effectiveness of due diligence policy and measures,

- Combatting climate change.

Scope of the CSDDD

>1,000 employees

€450 million turnover globally

No employee threshold

€450 million turnover in the EU

EU: >1,000 employees

Non-EU: no employee threshold

EU and non-EU: €80 million turnover

EU and non-EU: €22.5 million in royalties

The above thresholds are applicable if they are achieved by companies annually for two consecutive fiscal years. Responsibilities must be fulfilled either by the parent company or by a specified subsidiary in case the ultimate parent is a holding company that does not participate in managing financial or operational decisions for the group or its individual entities.

All EU and non-EU companies meeting the relevant thresholds must conduct due diligence across their chains of operations, concentrating on their own activities and upstream operations. A defined range of downstream activities, such as product distribution, transportation, and storage, are also encompassed.

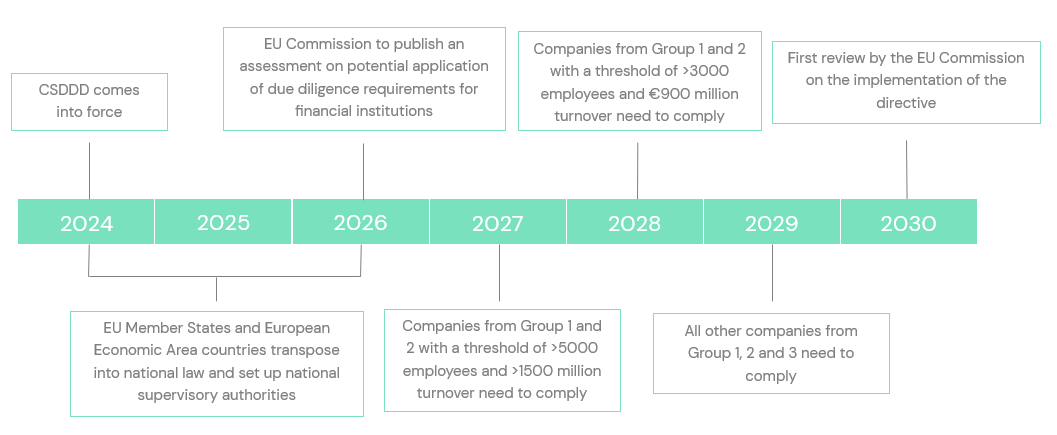

Implementation Timeline

The CSDDD will be enforced with a phase-in approach based on company size and turnover, starting three years from entry into force. Companies will be categorised as follows:

- From 2027: 3-year period for companies with over 5000 employees and €1500 million turnover,

- From 2028: 4-year period for those with over 3000 employees and €900 million turnover,

- From 2029: 5-year period for companies with over 1000 employees and €450 million turnover, and for companies having entered into franchising or licensing agreements with over €80 million turnover in the EU and €22.5 million in royalties.

EU Member States have a two-year window from the date of enforcement to incorporate the directive into their national legislation. Additionally, they must establish supervisory bodies and undertake suitable measures to enforce the provisions of the CSDDD.

The directive mandates the EU Commission to evaluate the necessity of crafting customised due diligence standards for companies involved in financial services and investment activities. This evaluation will take into account the existing legislative frameworks applicable to regulated financial entities. The findings of this assessment must be reported by May 2026.

Next Steps

While compliance for companies will commence in 2027, the process of designing and implementing due diligence is intricate and time-consuming. The following are several crucial steps businesses should contemplate taking in preparation:

- An assessment of the company’s current state,

- Engage internal stakeholders and identify their roles and responsibilities,

- Value chain mapping and risk prioritisation,

- A roadmap for implementation.